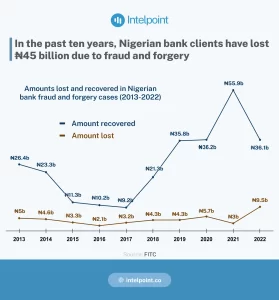

Nigerian Banks Face ₦42.6 Billion Fraud Losses in Three Months

Recent reports reveal that Nigerian banks lost ₦42.6 billion to fraud in just three months. This staggering figure highlights a growing crisis in the financial sector. As digital banking becomes more popular, fraudsters are finding new ways to exploit vulnerabilities, leading to significant financial losses for banks and their customers.

The Nigeria Inter-Bank Settlement System (NIBSS) released the report, detailing various types of fraud. Cybercrime, identity theft, and insider fraud are at the forefront of these issues. One major incident involved a bank that lost ₦5 billion due to a cyber attack. Hackers gained access to customer accounts, draining funds before the bank could respond.

Experts point to several reasons for this surge in fraud. Many banks still lack adequate cybersecurity measures. Additionally, employee training is often insufficient. The rapid rise of digital banking without proper security upgrades has left banks vulnerable. Dr. Aisha Bello, a cybersecurity analyst, states, “Many banks are still playing catch-up when it comes to securing their systems.” The speed of technological change means fraudsters are always looking for new weaknesses to exploit.

The COVID-19 pandemic accelerated the shift to online banking. Many customers now prefer digital transactions over traditional methods. This shift has created a perfect environment for fraud. A recent survey found that 70% of Nigerians experienced some form of fraud while using online banking services. This statistic raises serious concerns about the safety of digital transactions.

In response, banks are investing in advanced security technologies. Many institutions are now using artificial intelligence (AI) and machine learning to monitor transactions in real-time. These technologies help identify suspicious activities quickly. For example, a leading bank implemented an AI-driven fraud detection system that reduced fraudulent transactions by 30% in just one quarter.

However, technology alone cannot solve the problem. A comprehensive approach is necessary, including employee training and customer education. Banks must ensure their staff can identify potential fraud. Customers also need to understand the risks associated with online banking. “Education is key,” says Dr. Bello. “Customers need to know how to protect themselves and recognize warning signs of fraud.”

Regulatory bodies are also increasing their efforts to combat financial fraud. The Central Bank of Nigeria (CBN) has introduced stricter regulations aimed at enhancing banking security. These regulations require banks to adopt robust security measures. They must also report any fraudulent activities promptly. Noncompliance can lead to hefty fines, motivating banks to prioritize security.

The implications of these fraud losses extend beyond individual banks. They impact the entire economy. Cumulatively, such losses can lead to increased banking fees and reduced lending capacity. This situation can slow down economic growth. As banks deal with the financial fallout from fraud, they may pass on costs to consumers. This could further strain the relationship between banks and their customers.

As the financial landscape evolves, the fight against fraud requires a concerted effort from all stakeholders. The recent report serves as a wake-up call for the banking sector. It highlights the urgent need for a proactive approach to security. With fraudsters becoming more sophisticated, complacency is no longer an option. Banks must adopt a multifaceted strategy that includes technology, education, and regulatory compliance to protect their operations and restore customer trust.

The road ahead may be challenging. However, with the right measures in place, the banking sector can emerge stronger. The losses incurred in the past three months should not be seen merely as setbacks. Instead, they present an opportunity for banks to reassess their security protocols. They can reinforce their commitment to protecting customer assets.

In conclusion, as Nigerian banks navigate this turbulent landscape, the focus must remain on creating a secure banking environment. Prioritizing customer safety and confidence is essential. Only then can the sector hope to recover from the significant losses incurred and build a robust defense against future threats.

{kind=link}