Nigerian Banking Fraud Triples in 2023: NIBSS Sounds Alarm

Sharp Rise in Financial Crimes Sparks Nationwide Concern

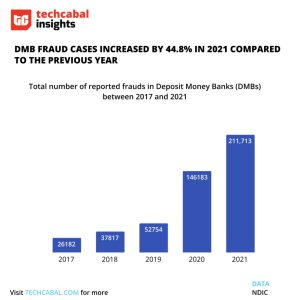

Nigeria’s banking sector faces an unprecedented crisis as new data reveals a staggering 300% increase in financial fraud cases during 2023. The Nigeria Inter-Bank Settlement System (NIBSS), the nation’s central financial infrastructure provider, has issued an urgent warning about this alarming trend that threatens both institutional stability and consumer trust.

Fraud Patterns and Vulnerable Targets

Recent analysis shows criminals exploiting multiple channels:

- Mobile banking platforms (42% of cases)

- Online payment gateways (33% of cases)

- Traditional branch transactions (25% of cases)

Common Fraud Tactics Exposed

Security experts identify four primary attack methods:

1. Social Engineering Scams

Fraudsters impersonate bank officials through sophisticated phishing campaigns. Last month, a coordinated attack drained ₦78 million from 132 customers within 72 hours.

2. Identity Theft Syndicates

Criminal networks harvest personal data through compromised databases. The Economic and Financial Crimes Commission (EFCC) recently busted a ring operating across six states.

3. ATM Skimming Operations

Physical card compromises remain prevalent. NIBSS reports 17,000 compromised cards in Q1 2023 alone.

Video: Demonstration of how criminals install skimming devices on ATMs.

Economic Impact and Consumer Fallout

The fraud surge carries significant consequences:

- ₦9.8 billion lost in H1 2023 (Central Bank of Nigeria)

- 34% decrease in mobile banking adoption since January

- 22% rise in cash withdrawal requests at branches

Institutional Responses and Security Measures

Financial institutions are implementing new safeguards:

Enhanced Authentication Protocols

Banks now require multi-factor authentication for transactions above ₦50,000. Some institutions have introduced voice recognition systems.

Customer Education Initiatives

Nigerian major banks have launched nationwide awareness campaigns. “Never share your BVN or OTP with anyone,” warns First Bank’s current TV spot.

Regulatory Crackdown Intensifies

The Central Bank of Nigeria has announced strict new measures:

- Mandatory fraud reporting within 24 hours

- ₦5 million fine for delayed incident disclosure

- Quarterly security audits for all financial institutions

Consumer Protection Strategies

Banking experts recommend these safety practices:

- Enable transaction alerts for all accounts

- Use biometric authentication where available

- Regularly review account statements

- Report suspicious activity immediately

Future Outlook and Industry Predictions

While NIBSS projects fraud rates will stabilize by Q2 2024, cybersecurity firms warn of emerging threats:

- AI-powered phishing tools

- Deepfake voice scams

- Cryptocurrency-based money laundering

The Nigerian banking sector stands at a critical juncture. As digital transactions grow, so does the battle against financial crime. Industry leaders emphasize that combating this wave requires cooperation between institutions, regulators, and customers alike.

{kind=link}